Division of Labor vs. the Invisible Hand

Division of Labor vs. the Invisible Hand

Two divergent trajectories of economic thought from two of its foundations

In my previous post, I took at long look at the division of labor in Adam Smith, and argued that it should perhaps be the centerpiece of economics. Many of the insights of economics are consequences of this idea, and it helps provide a framework to understand the complexity and nuance of modern society at a systems level.

Before moving on to more applications in future posts, I want to consider the other famous idea in Smith. He is most famous (or infamous, depending on your point of view) for the idea of the “invisible hand.” If anyone has heard of Smith at all, they him for this idea and often take it out of context, putting words into Smith’s mouth to fit their own priors.

One of the theses of my project here, at least in terms of the history of economic thought, is that elaboration of these two concepts about markets — (1) the division of labor and (2) the invisible hand — led to two very different trajectories for economics as a discipline over the past two and a half centuries.

The invisible hand has been extrapolated to become a provable theorem to show that markets lead to equilibrium where all gains from trade are exhausted and everything is optimal, situated in a world of diminishing returns (and other assumptions). Its apex is the neoclassical paradigm focuses almost exclusively on the marginal conditions that the invisible hand brings about in competitive equilibrium.

The oft-forgotten division of labor describes a world of increasing returns, where larger and more robust markets lead to increased specialization, innovation, and flourishing. Only in the last few decades has an alternate strand of economic (and other interdisciplinary) thinking emerged that considers the realm of increasing returns, innovation, and their connection to sustained economic growth. I aim to trace this alternate strand of thought of those who recognized the division of labor insight, but worked in the background, while diminishing returns and static efficiency reigned in the intellectual foreground.

Before proceeding, I hasten to add that I am not trying to make a mountain out of a molehill. The title of this post is a tad disingenuous, but now that I have your attention, I think this is a useful framework to compare different trajectories for economic analysis from two great foundational ideas. I definitively do not think that there is any tension between these ideas in Smith, nor do I think that the invisible hand is a trivial concept! These two ideas are complements, but economics profession has swung the pendulum in one direction at the expense of the other, so consider this a corrective to restore some balance.

On that note, I would also caution against swinging the pendulum too far in the opposite direction: as much as I may criticize equilibrium models and neoclassical approach to economics, I am not prepared to jettison them altogether, even if attractive alternatives are appearing on the horizon.

The Invisible Hand: Technical Models With An Institutional Filter

When teaching the technical tools of economics to my students, I like to take Smith’s famous paragraph in the Wealth of Nations about the invisible hand and highlight three passages within it:

"[Though] he intends only his own gain, and he is in this, as in many other cases, led by an invisible hand to promote an end which was no part of his intention…By pursuing his own interest he frequently promotes that of the society more effectually than when he really intends to promote it," (Book IV, Chapter 2.9).

The first passage I’ve highlighted — “[though] he intends only his own gain” — is a clear reference to the idea of self-interest (or if I must use that bugbear of a term, “rationality”).

The final passage I’ve highlighted — “he frequently promotes that [interest] of the society” — describes an outcome that is “good,” i.e. society is improved and experiences progress and prosperity. This is clearly implied to have been caused by people pursuing their own interests. But it should be clear that this outcome does not necessarily (i.e. always and everywhere) follow from the first observation, that people pursue their own self interest. There are clearly cases in society where self-interest doesn’t lead to good outcomes, cases like traffic jams, pollution, etc. I leave it as an exercise to the reader to consider others [pick your favorite complaint about modern economics, capitalism, etc.]

At the risk of oversimplifying, modern economics consists of two of primary models: (1) constrained optimization and (2) equilibrium. Without getting technical, “constrained optimization” means simply that “people do the best that they can” — i.e. try to accomplish their goals. Or to simplify, people are rational, self-interested, etc. The “solution” to the model is a choice where a person would not want to change what they are doing (there are no better alternatives), i.e. an “optimum.”

Equilibrium captures the fact that many such maximizing individuals are interacting amidst a world of scarcity — my plans or use of resources will conflict with yours, and so we need to mutually adjust our plans until we can both achieve some of our goals with our resources (and now extend this to n such persons). In many contexts, we may predict an outcome where such mutual adjustment stops, and nobody wants to change what they are doing (i.e. everyone is at an optimum!). This is called an equilibrium — a stable, predictable outcome where the system is “at rest,” at least until acted upon by some external force. Economists primarily focus on how prices adjust to attain equilibrium allocations of resources in markets: the famous supply and demand graph.

This is finally where the middle passage I’ve highlighted in Smith’s famous paragraph — “led by an invisible hand” — finally comes into play. If we merely define the invisible hand as a metaphor describing the alignment between self-interest and common good, this essentially is how modern economists tend to talk about the invisible hand.

The neoclassical project of the 20th century was to formalize and systematize this “invisible hand” theorem of aligning self-interest and common good with a series of equations (and for undergrads, graphs): Utility-maximizing individuals compete with one another to buy from profit-maximizing firms that compete with each other in a market that reaches an equilibrium of a single price where all individuals and firms have maximized their utility and profits; society produces all goods to the point where the social benefit of an additional unit being produced is perfectly balanced with the cost of producing it; profits are exactly zero, and the price of all goods is equal to their cost per unit. I admit, I still cannot help but admire the beauty of such an elegant system; but it is not the one we live in.

The apex of this mathematical and formalist approach was the famous Arrow-Debreu proof in the 1950s that equilibrium can exist for all possible markets under all possible contingencies simultaneously, at least under certain assumptions. Neoclassical economics has finally proved the invisible hand theorem definitively and mathematically (under certain conditions)! Or such is the received wisdom within the profession.

One downside of this approach is that it opens up economics to easy pot-shots from outsiders. Non-economists, pundits, and critics of capitalism equate the invisible hand with the contention that self-interest always and everywhere is supposed to lead to the common good, and only wicked people and (redundantly) economists believe this nonsense. Economists purportedly put religious-like faith that The Market Will Provide, always and everywhere. Sometimes this is extended to the belief in a literal hand, i.e. the hand of God, that naturally orders things under capitalism and thus must not be challenged. (Here is just one example of a current unfortunate controversy about this).

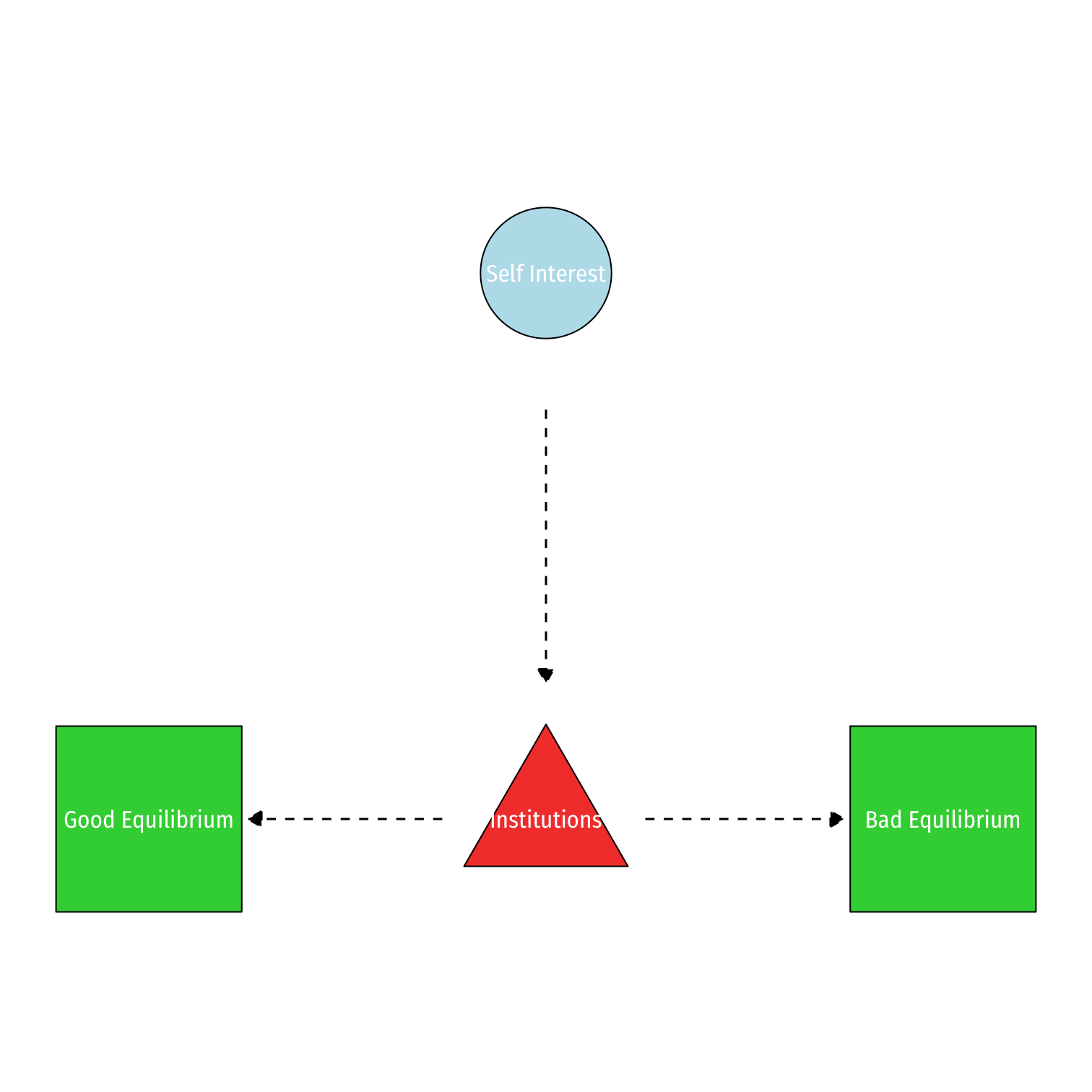

Put aside religion and consider the invisible hand for what it is, a metaphor that summarizes very complex ideas and relationships. Now if we return to the two other phrases in bold: that people act in their self-interest, and this tends to better society. We’ve already seen how self-interest obviously does not always and everywhere promote the common good. So this opens up a fundamental question, one that economics really is about: how do we channel self-interest to attain good social outcomes and avoid bad ones? The answer is institutions: “good” institutions channel self-interest into productive outcomes; “bad” institutions channel self-interest into unproductive or even destructive outcomes for society. One of my all time favorite papers by William Baumol argues exactly this. As Peter Boettke best summarizes it (a bit more technically than I’ve allowed for here), we derive the invisible hand theorem from the rational choice postulate via institutional analysis. I like to show the relationship between these three ideas and passages in Smith with the following diagram:

Answering just what are “good” and “bad” institutions exactly is the million dollar question. But back to my ultimate point: one of the central institutions is the division of labor, which is limited by the extent of the market. Not at all to denigrate the invisible hand as a concept, but I think it still proceeds from the division of labor idea (and more specifically Smith’s insight that it is spontaneously ordered), as most economics does. (Textually, also, the quote with in-passing mention of the invisible hand doesn’t come until near the end of the book when Smith is criticizing mercantilism in Book IV; Division of Labor is the first concept in Wealth of Nations!)

"The oft-forgotten division of labor describes a world of increasing returns"

The increasing returns of the DoL is "limited by the extent of the market", suggesting increasing returns could be a local not global phenomenon (under existing conditions). For IR to be global, you'd need to argue that markets possess the potential for limitlessness. Or, which is the same thing, that greater specialization itself enables market expansion. At that point you have recursion and turtles all the way down. Which is fine, it just makes things messy.

"Textually, also, the quote with in-passing mention of the invisible hand doesn’t come until near the end of the book when Smith is criticizing mercantilism in Book IV; Division of Labor is the first concept in Wealth of Nations!"

Ah, but the IH appears in TMS, published 17 years earlier than WN, also making a claim about the distribution of the necessaries of life. You'll want to look at that passage because it sure doesn't seem like he's suggesting good institutions are necessary for the IH to operate for public benefit. TMS IV.i.10

There was a conversation between Gavin Kennedy, Craig Smith, Dan Klein, and Brandon Lucas about the IH centrality. See "The Centrality of the Invisible Hand in Smith's Books" Kennedy (2010), and "On the Deliberate Centrality of an Invisible Hand" Klein and Lucas (2011)